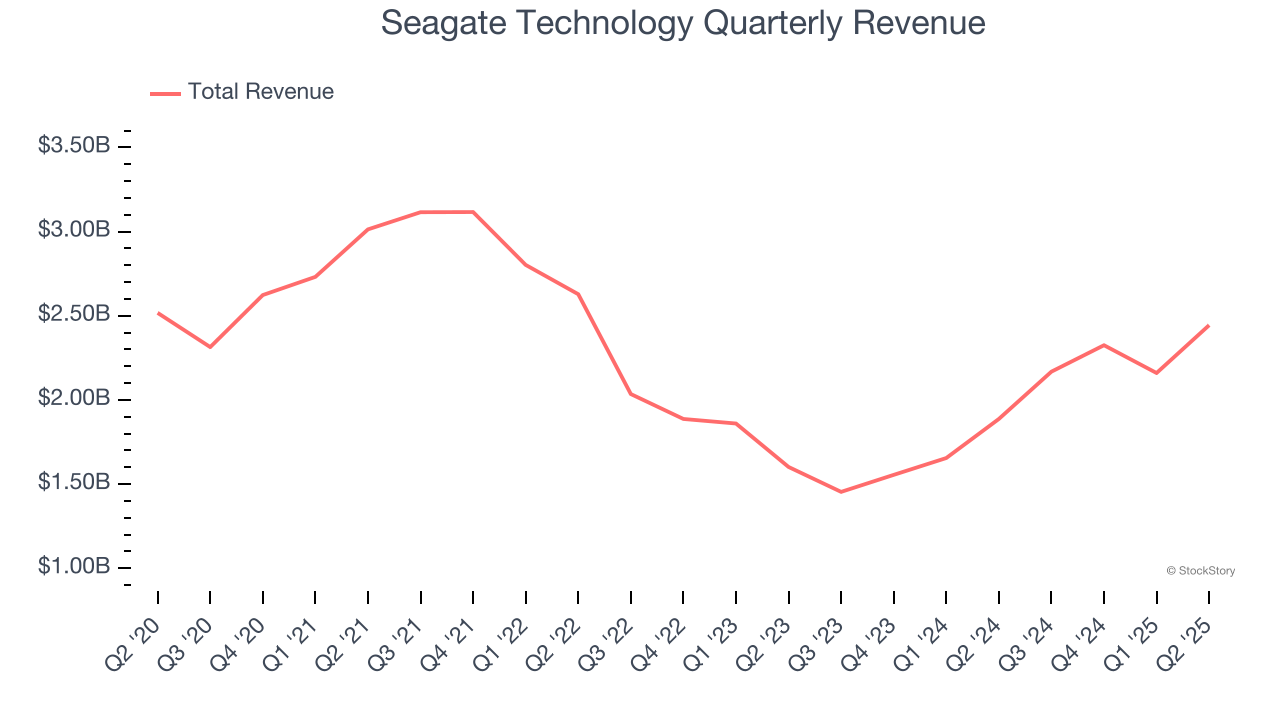

Data storage manufacturer Seagate (NASDAQ:STX) announced better-than-expected revenue in Q2 CY2025, with sales up 29.5% year on year to $2.44 billion. On the other hand, next quarter’s revenue guidance of $2.5 billion was less impressive, coming in 2.5% below analysts’ estimates. Its non-GAAP profit of $2.59 per share was 6% above analysts’ consensus estimates.

Is now the time to buy Seagate Technology? Find out by accessing our full research report, it’s free.

Seagate Technology (STX) Q2 CY2025 Highlights:

- Revenue: $2.44 billion vs analyst estimates of $2.43 billion (29.5% year-on-year growth, 0.6% beat)

- Adjusted EPS: $2.59 vs analyst estimates of $2.44 (6% beat)

- Adjusted EBITDA: $697 million vs analyst estimates of $699 million (28.5% margin, in line)

- Revenue Guidance for Q3 CY2025 is $2.5 billion at the midpoint, below analyst estimates of $2.56 billion

- Adjusted EPS guidance for Q3 CY2025 is $2.30 at the midpoint, below analyst estimates of $2.32

- Operating Margin: 23.2%, up from 16.6% in the same quarter last year

- Free Cash Flow Margin: 17.4%, down from 20.1% in the same quarter last year

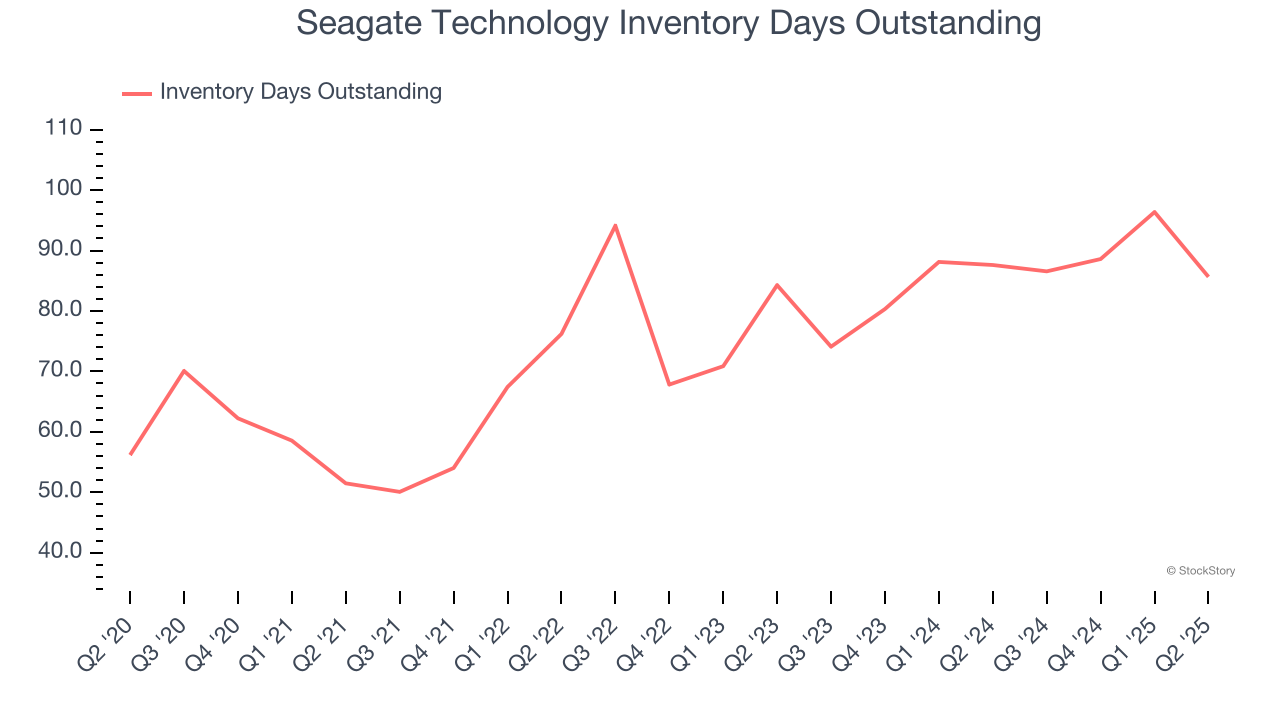

- Inventory Days Outstanding: 86, down from 96 in the previous quarter

- Market Capitalization: $31.93 billion

"Seagate’s strong FQ4 performance underscores our commitment to profitable growth, marked by a 30% year-over-year revenue increase, record gross margin, and non-GAAP EPS expanding to the top of our guidance range. These achievements reflect the structural enhancements we’ve implemented in our business and ongoing demand strength from cloud customers for our high-capacity drives," said Dave Mosley, Seagate’s chief executive officer.

Company Overview

The developer of the original 5.25inch hard disk drive, Seagate (NASDAQ:STX) is a leading producer of data storage solutions, including hard drives and Solid State Drives (SSDs) used in PCs and data centers.

Revenue Growth

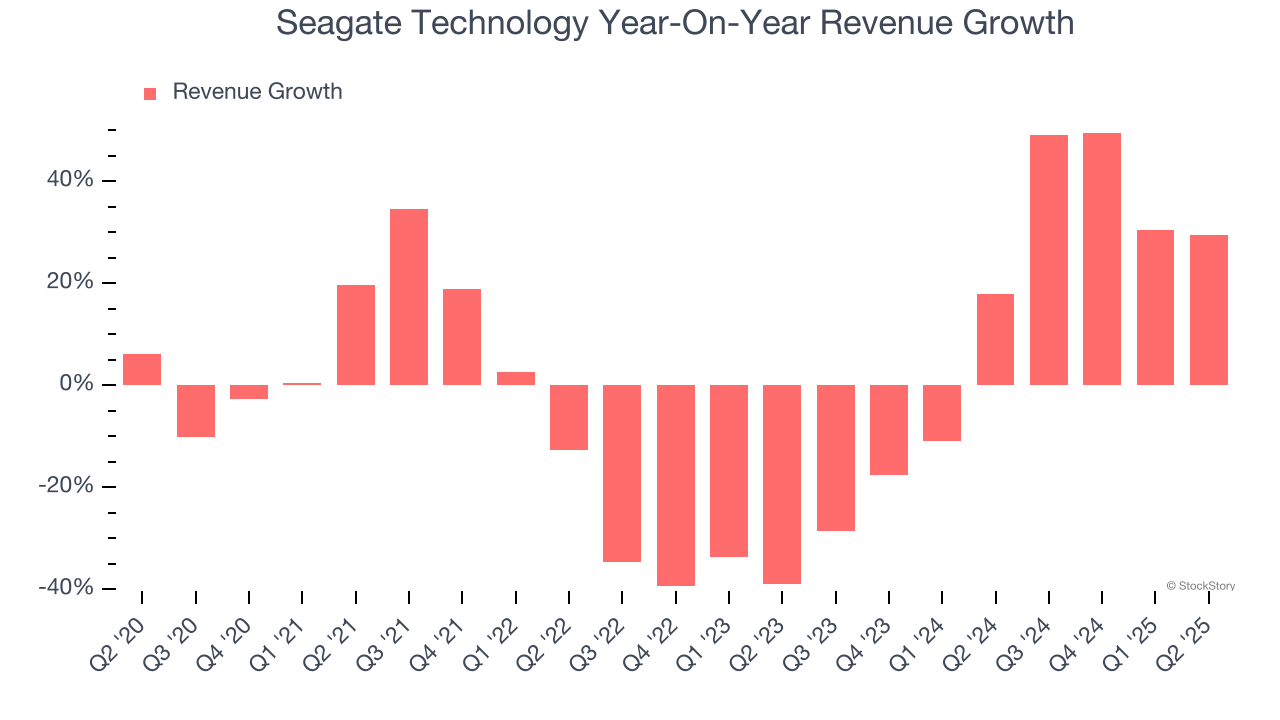

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Seagate Technology struggled to consistently generate demand over the last five years as its sales dropped at a 2.8% annual rate. This was below our standards and is a tough starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Seagate Technology’s annualized revenue growth of 11% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Seagate Technology reported robust year-on-year revenue growth of 29.5%, and its $2.44 billion of revenue topped Wall Street estimates by 0.6%. Beyond the beat, this marks 5 straight quarters of growth, implying that Seagate Technology is in the middle of its cycle - a typical upcycle generally lasts 8-10 quarters. Company management is currently guiding for a 15.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 15.2% over the next 12 months, an improvement versus the last two years. This projection is admirable and implies its newer products and services will catalyze better top-line performance.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Seagate Technology’s DIO came in at 86, which is 11 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

Key Takeaways from Seagate Technology’s Q2 Results

We were impressed by Seagate Technology’s strong improvement in inventory levels. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its both revenue and EPS guidance for next quarter missed, and this is weighing on shares. The stock traded down 7% to $142.25 immediately after reporting.

So do we think Seagate Technology is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.