MGIC Investment has been treading water for the past six months, recording a small return of 3.8% while holding steady at $25.72.

Is there a buying opportunity in MGIC Investment, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is MGIC Investment Not Exciting?

We're swiping left on MGIC Investment for now. Here are three reasons why MTG doesn't excite us and a stock we'd rather own.

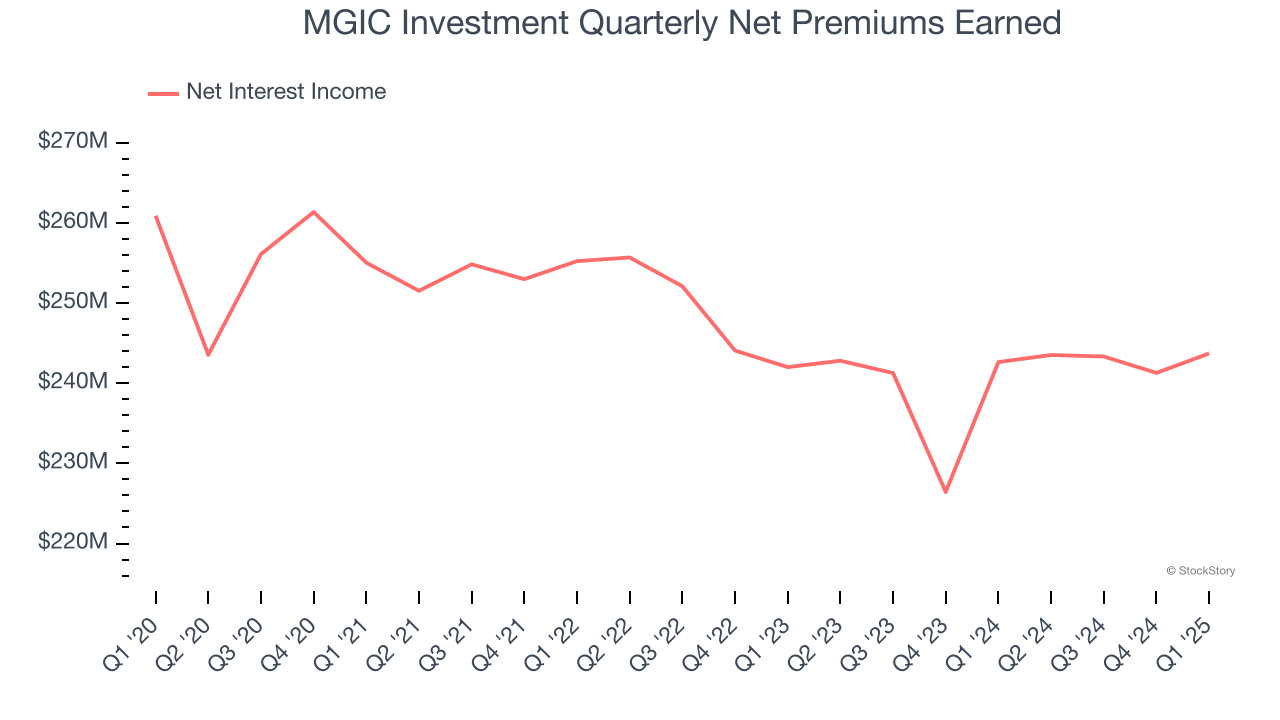

1. Declining Net Premiums Earned Reflects Weakness

Our experience and research show the market cares primarily about an insurer’s net premiums earned growth as investment and fee income are considered more susceptible to market volatility and economic cycles.

MGIC Investment’s net premiums earned has declined by 1.1% annually over the last four years, much worse than the broader insurance industry.

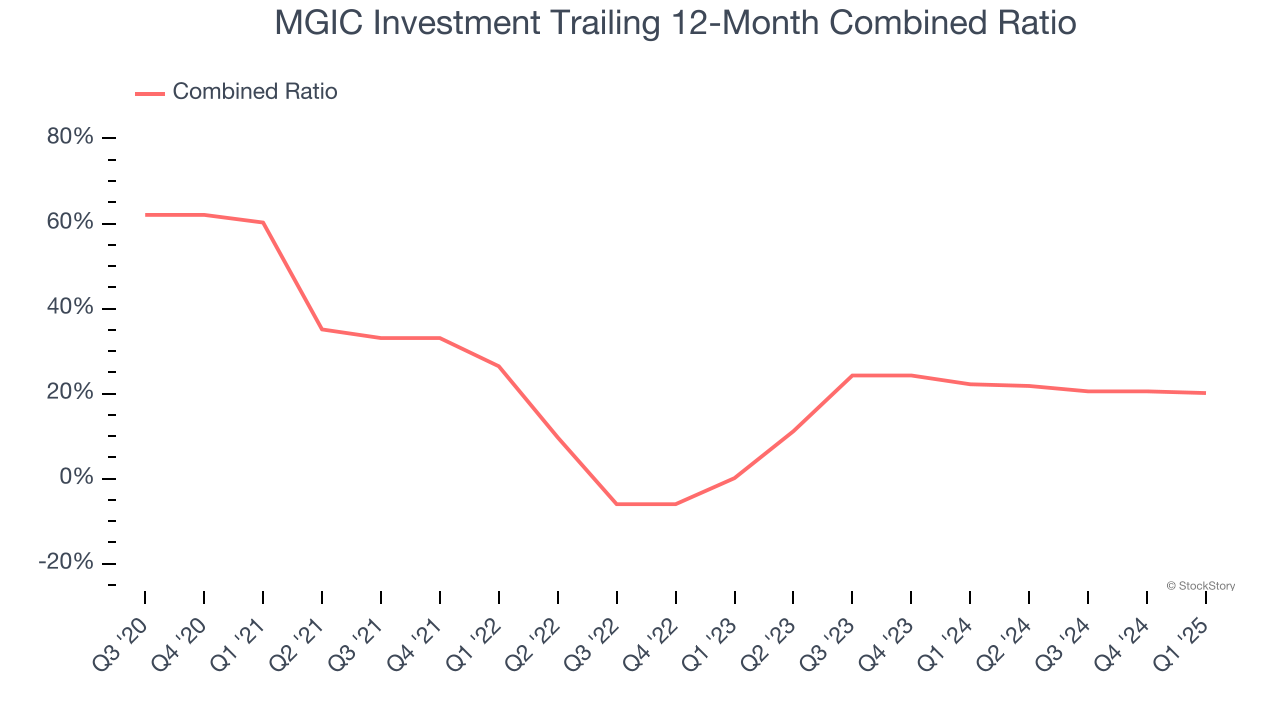

2. Deteriorating Combined Ratio

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at the combined ratio rather than the operating expenses and margins that define sectors such as consumer, tech, and industrials.

The combined ratio is:

- The costs of underwriting (salaries, commissions, overhead) + what an insurer pays out in claims, all divided by net premiums earned

If a company boasts a combined ratio under 100%, it is underwriting profitably. If above 100%, it is losing money on its core operations of selling insurance policies.

Over the last four years, MGIC Investment’s combined ratio has decreased by 40.1 percentage points, clocking in at 20.1% for the past 12 months. Said differently, the company’s expenses have grown at a slower rate than revenue, which is always a positive sign.

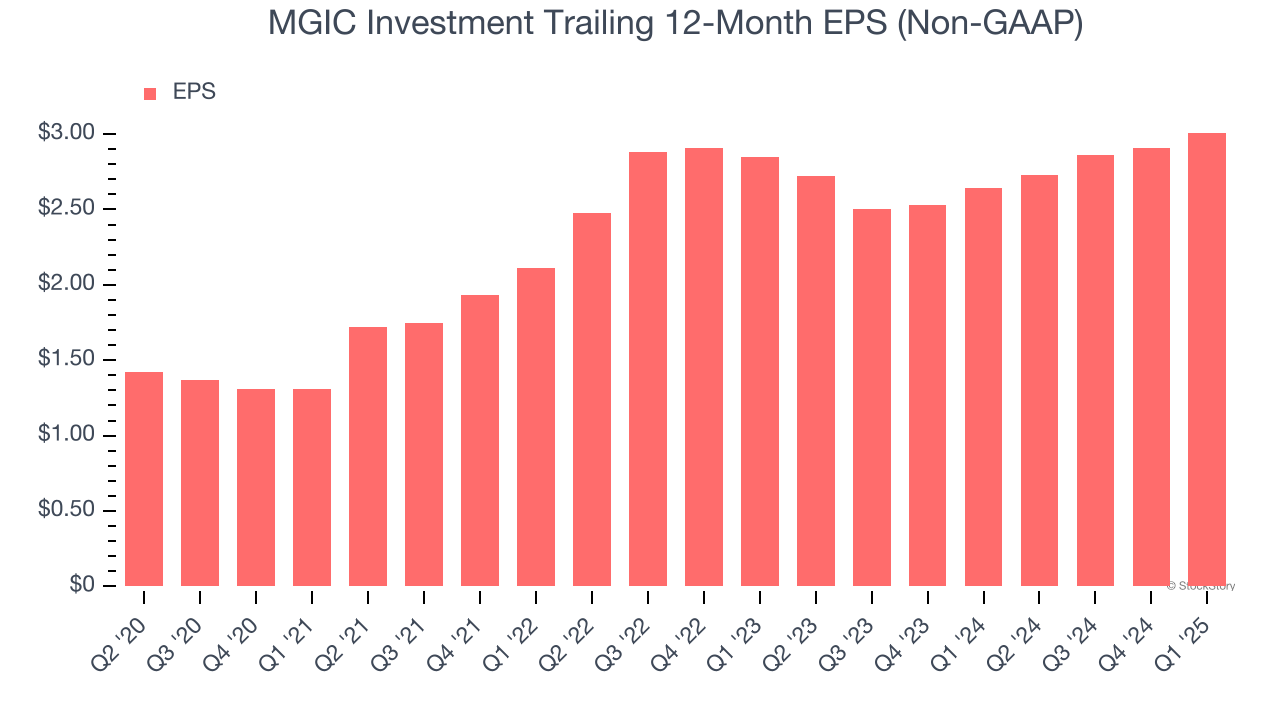

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

MGIC Investment’s weak 2.8% annual EPS growth over the last two years aligns with its revenue trend. This tells us it maintained its per-share profitability as it expanded.

Final Judgment

MGIC Investment isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 1.1× forward P/B (or $25.72 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

Stocks We Like More Than MGIC Investment

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.