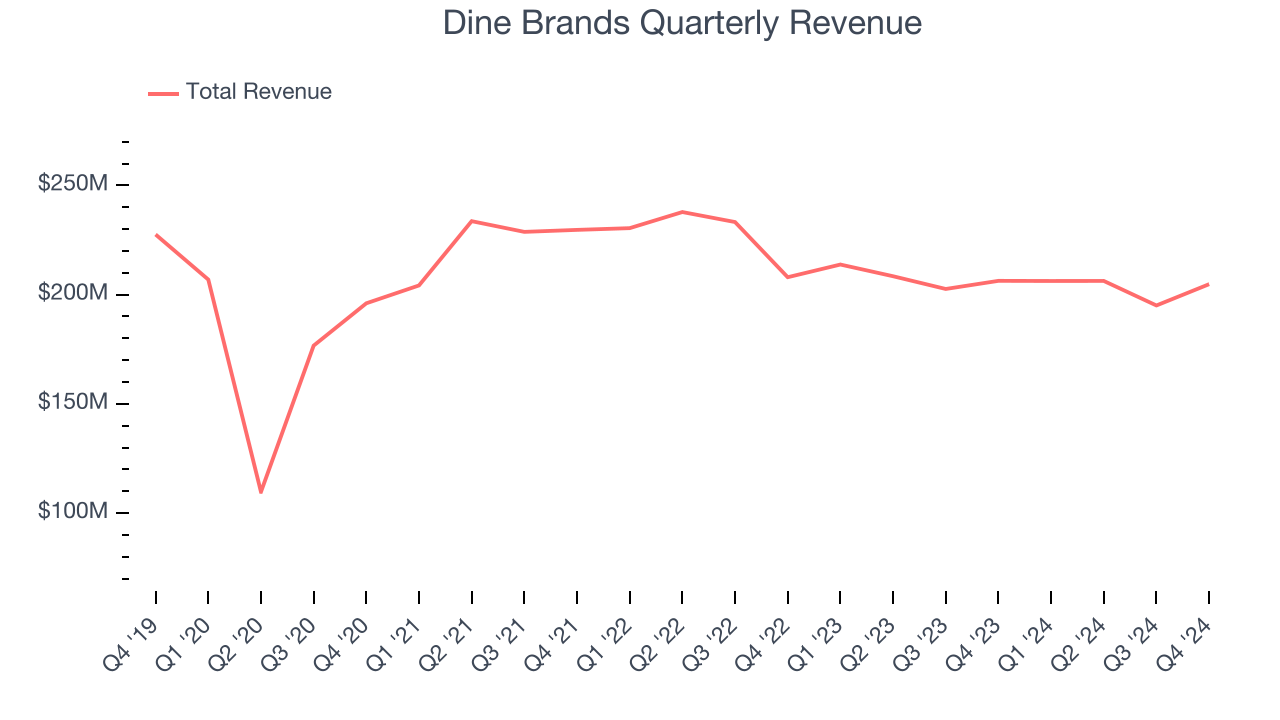

Casual restaurant chain Dine Brands (NYSE:DIN) reported Q4 CY2024 results topping the market’s revenue expectations, but sales were flat year on year at $204.8 million. Its non-GAAP profit of $0.87 per share was 35.4% below analysts’ consensus estimates.

Is now the time to buy Dine Brands? Find out by accessing our full research report, it’s free.

Dine Brands (DIN) Q4 CY2024 Highlights:

- Revenue: $204.8 million vs analyst estimates of $200.9 million (flat year on year, 1.9% beat)

- Adjusted EPS: $0.87 vs analyst expectations of $1.35 (35.4% miss)

- Adjusted EBITDA: $50.06 million vs analyst estimates of $58.44 million (24.4% margin, 14.3% miss)

- EBITDA guidance for the upcoming financial year 2025 is $240 million at the midpoint, below analyst estimates of $244.1 million

- Free Cash Flow Margin: 13%, down from 22.6% in the same quarter last year

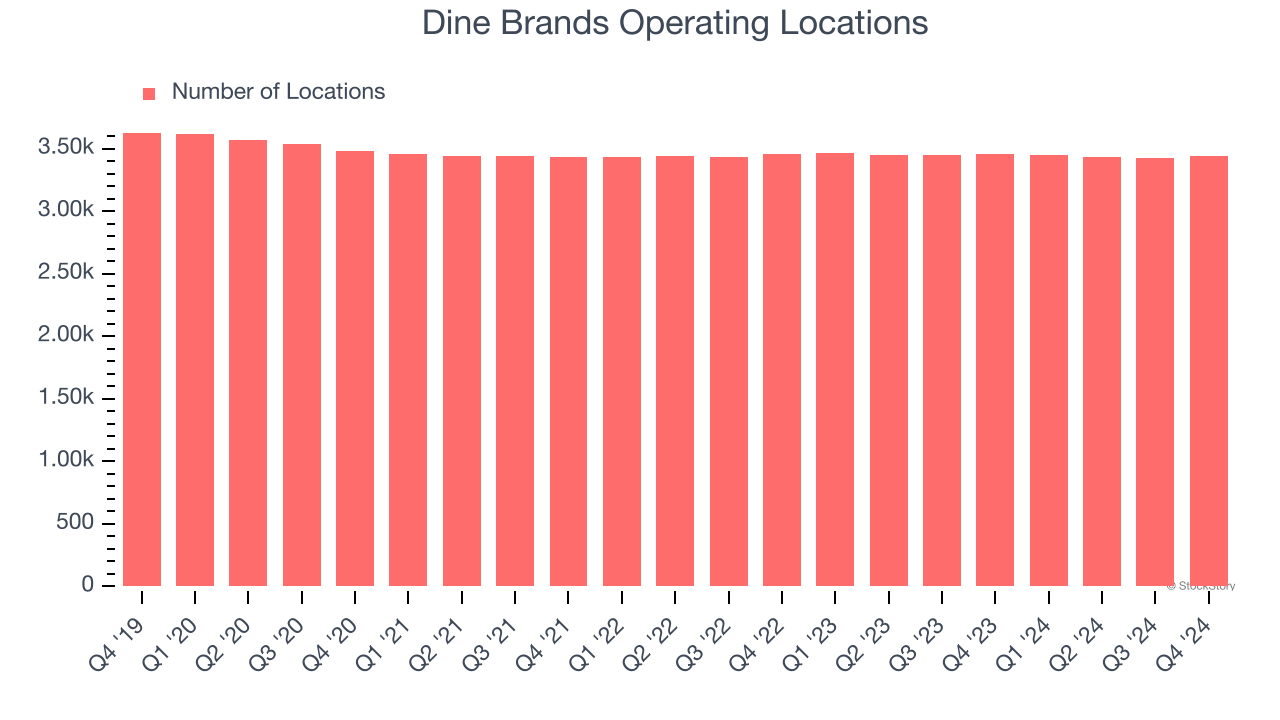

- Locations: 3,438 at quarter end, down from 3,456 in the same quarter last year

- Market Capitalization: $357.8 million

Company Overview

Operating a franchise model, Dine Brands (NYSE:DIN) is a casual restaurant chain that owns the Applebee’s and IHOP banners.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years.

With $812.3 million in revenue over the past 12 months, Dine Brands is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Dine Brands struggled to generate demand over the last five years (we compare to 2019 to normalize for COVID-19 impacts). Its sales dropped by 2.2% annually as it didn’t open many new restaurants.

This quarter, Dine Brands’s $204.8 million of revenue was flat year on year but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer menu offerings will fuel better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Dine Brands operated 3,438 locations in the latest quarter, and over the last two years, has kept its restaurant count flat while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

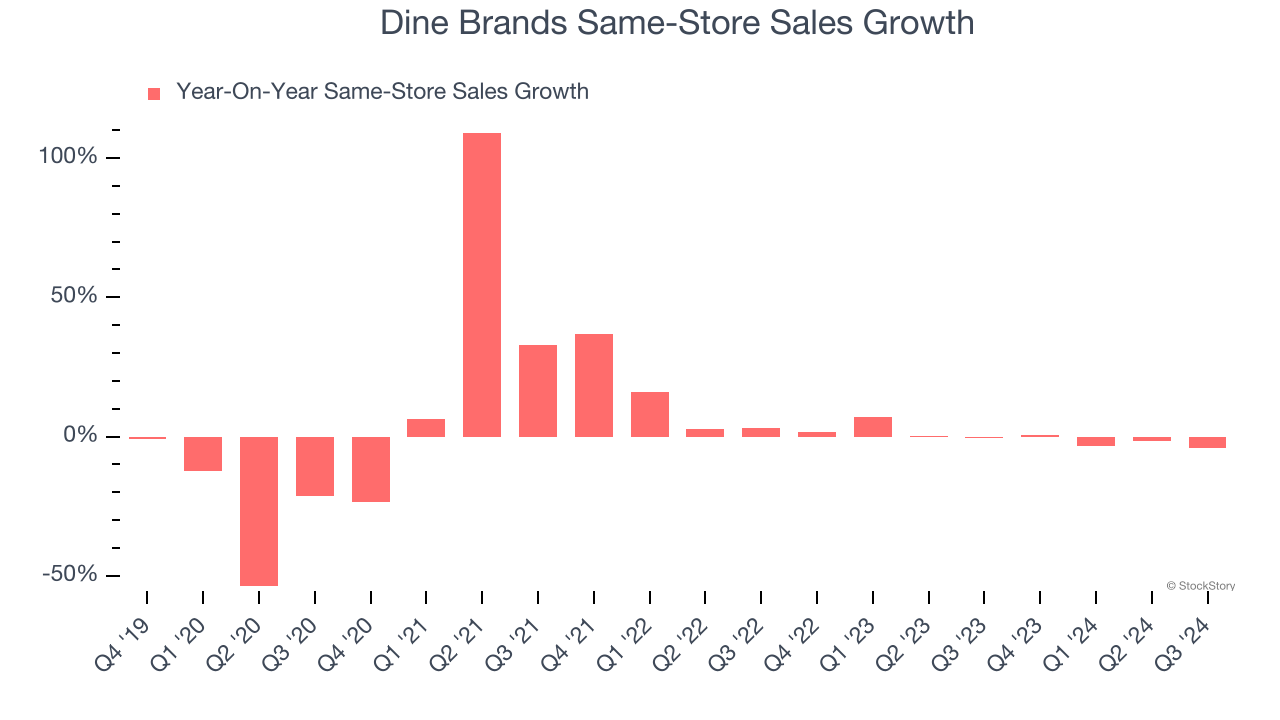

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Dine Brands’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Dine Brands starts opening new restaurants to artificially boost revenue growth.

Note that Dine Brands reports its same-store sales intermittently, so some data points are missing in the chart below.

Key Takeaways from Dine Brands’s Q4 Results

We enjoyed seeing Dine Brands beat analysts’ revenue expectations this quarter. On the other hand, its EPS fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock traded up 4.5% to $24.55 immediately after reporting.

So should you invest in Dine Brands right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.