Since September 2024, Union Pacific has been in a holding pattern, posting a small loss of 1.9% while floating around $247.85. The stock also fell short of the S&P 500’s 3.8% gain during that period.

Is now the time to buy Union Pacific, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're swiping left on Union Pacific for now. Here are three reasons why UNP doesn't excite us and a stock we'd rather own.

Why Do We Think Union Pacific Will Underperform?

Part of the transcontinental railroad project, Union Pacific (NYSE:UNP) is a freight transportation company that operates a major railroad network.

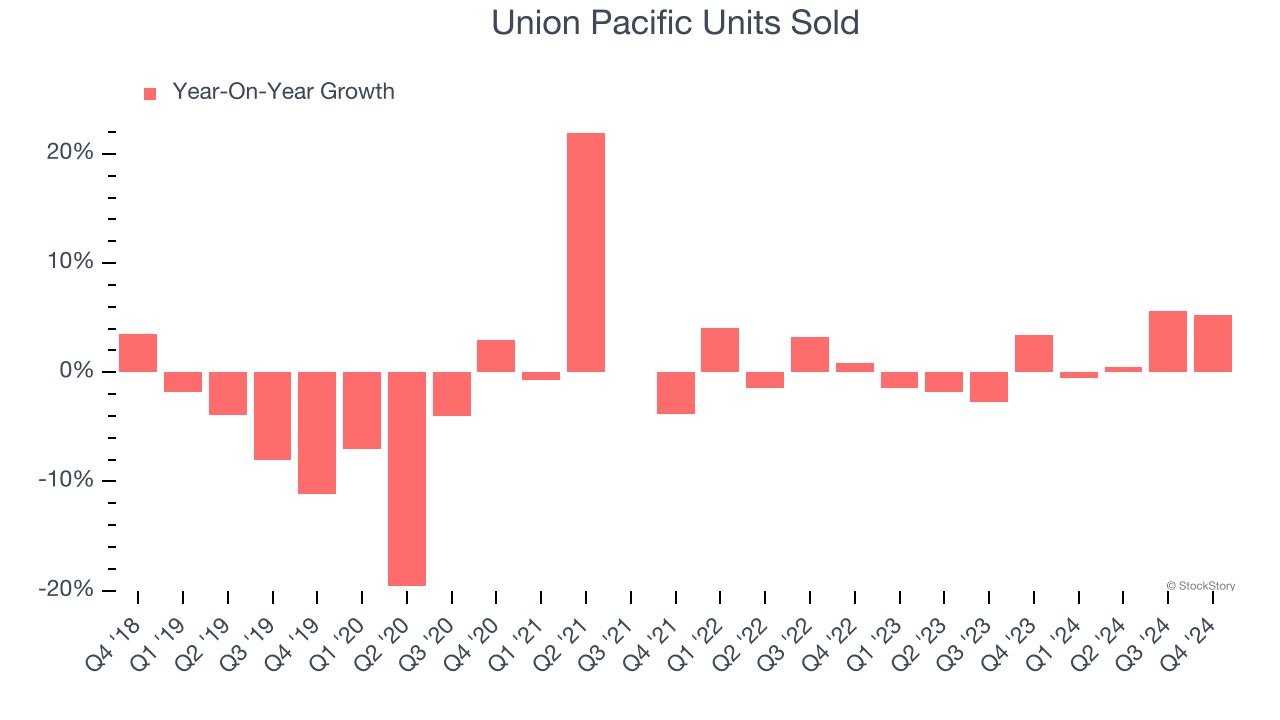

1. Weak Sales Volumes Indicate Waning Demand

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Rail Transportation company because there’s a ceiling to what customers will pay.

Over the last two years, Union Pacific’s units sold averaged 1% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

2. EPS Barely Growing

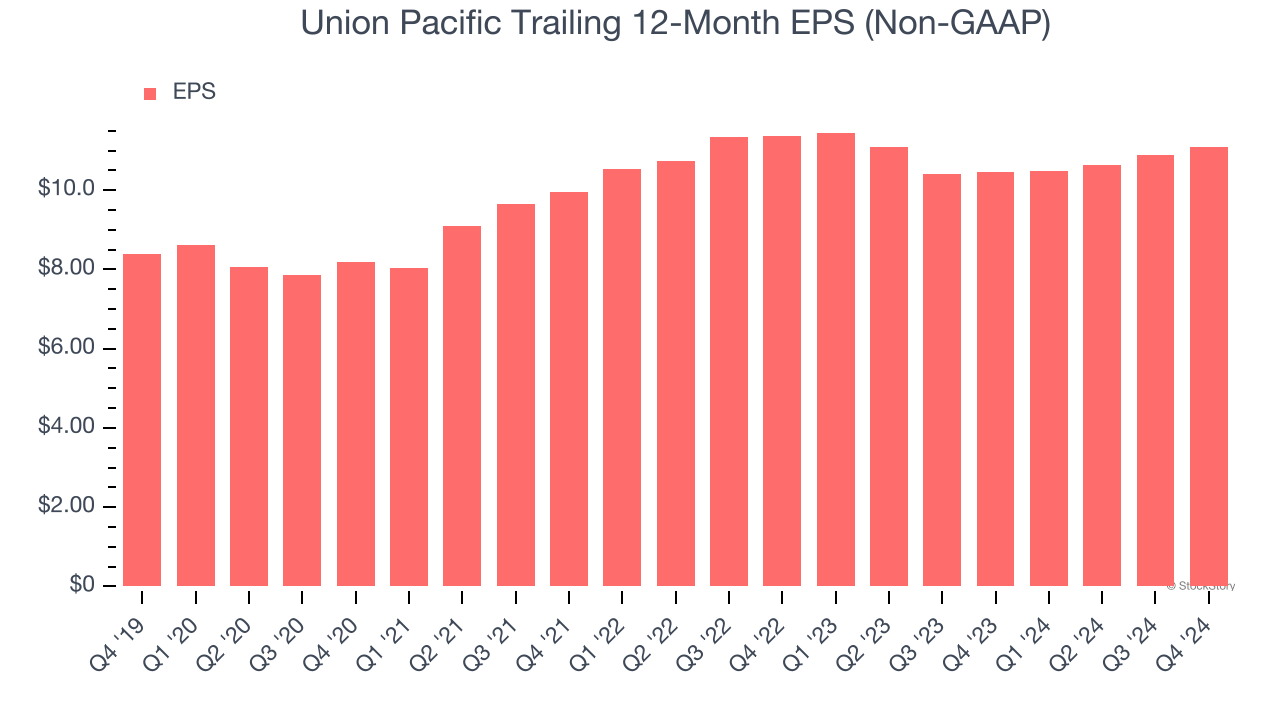

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Union Pacific’s EPS grew at an unimpressive 5.7% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 2.2% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

3. Free Cash Flow Margin Dropping

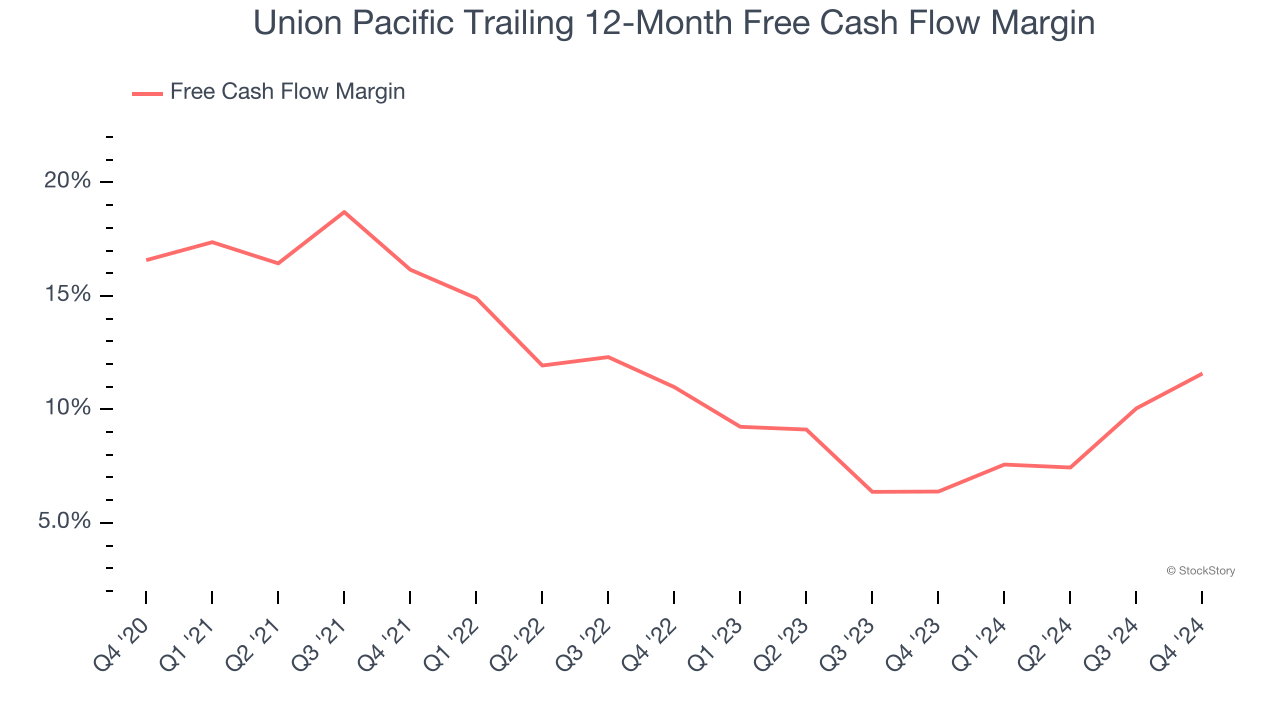

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Union Pacific’s margin dropped by 5 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal higher capital intensity and investment needs. Union Pacific’s free cash flow margin for the trailing 12 months was 11.6%.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of Union Pacific, we’ll be cheering from the sidelines. With its shares lagging the market recently, the stock trades at 20.7× forward price-to-earnings (or $247.85 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d suggest looking at one of our top digital advertising picks.

Stocks We Like More Than Union Pacific

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.