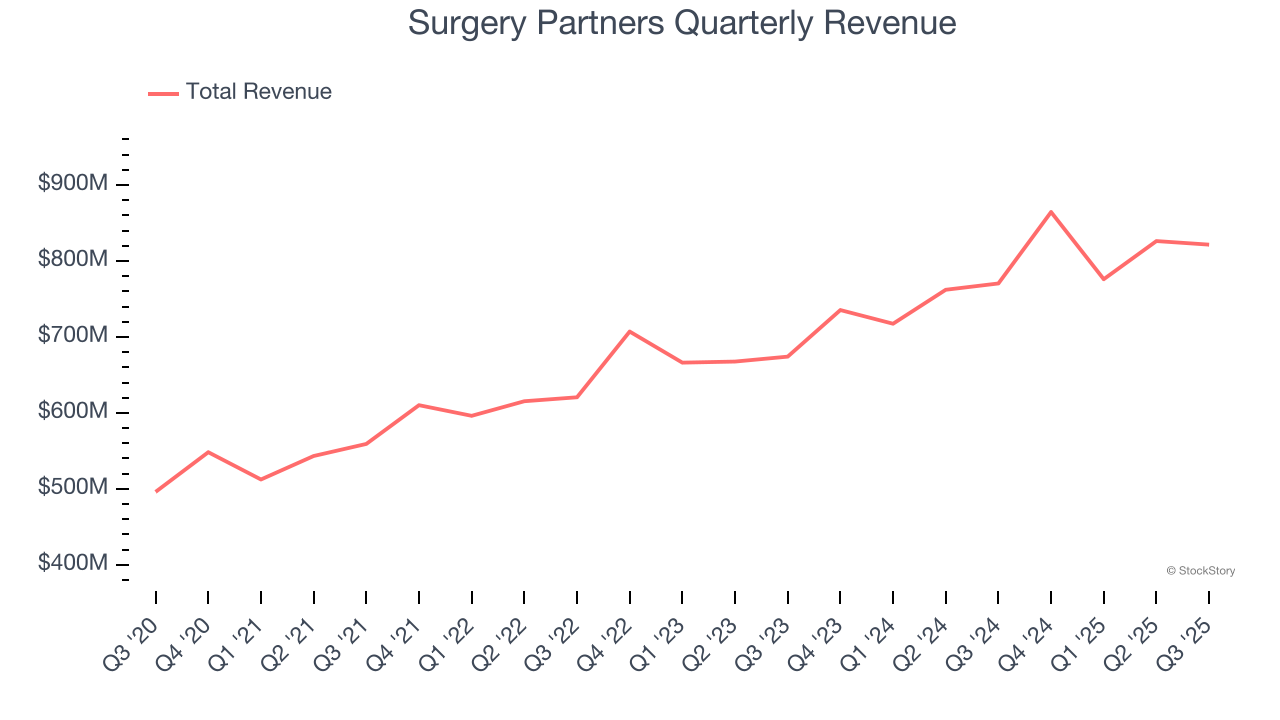

Healthcare company Surgery Partners (NASDAQ:SGRY) met Wall Streets revenue expectations in Q3 CY2025, with sales up 6.6% year on year to $821.5 million. On the other hand, the company’s full-year revenue guidance of $3.29 billion at the midpoint came in 2% below analysts’ estimates. Its non-GAAP profit of $0.13 per share was 19% below analysts’ consensus estimates.

Is now the time to buy Surgery Partners? Find out by accessing our full research report, it’s free for active Edge members.

Surgery Partners (SGRY) Q3 CY2025 Highlights:

- Revenue: $821.5 million vs analyst estimates of $821.8 million (6.6% year-on-year growth, in line)

- Adjusted EPS: $0.13 vs analyst expectations of $0.16 (19% miss)

- Adjusted EBITDA: $136.4 million vs analyst estimates of $136.2 million (16.6% margin, in line)

- The company dropped its revenue guidance for the full year to $3.29 billion at the midpoint from $3.38 billion, a 2.6% decrease

- EBITDA guidance for the full year is $537.5 million at the midpoint, below analyst estimates of $556.1 million

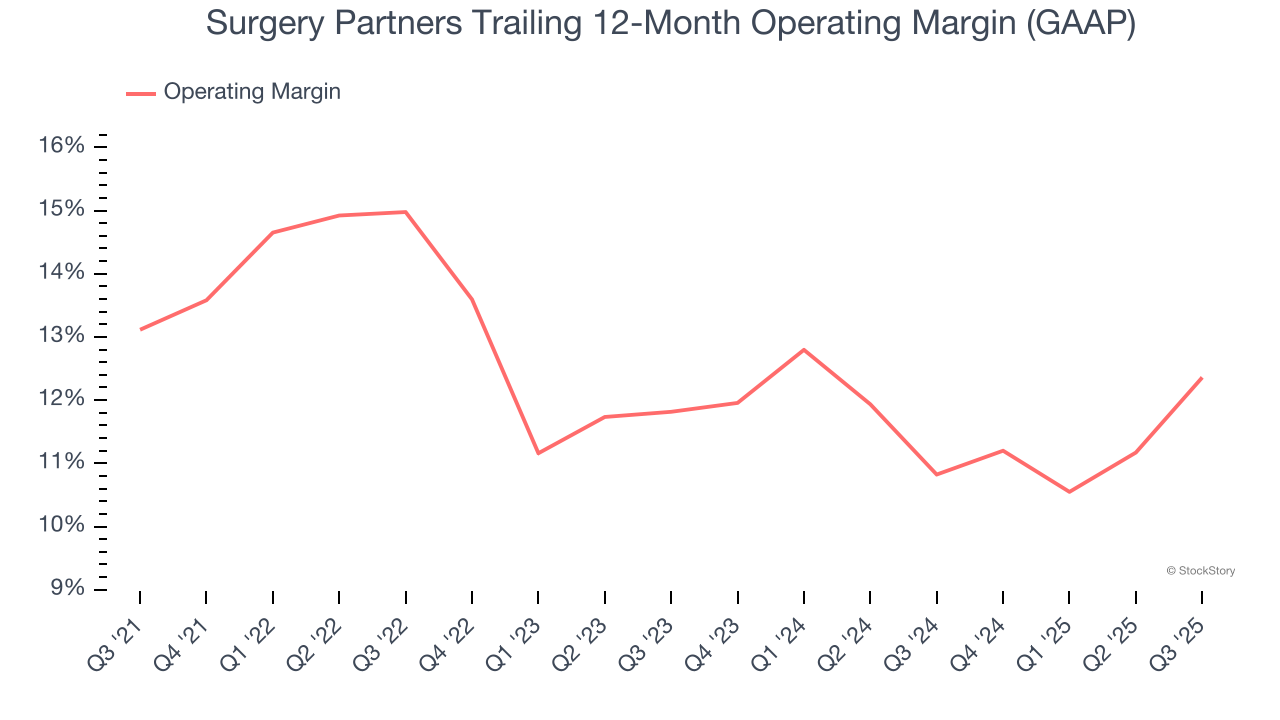

- Operating Margin: 12.9%, up from 7.9% in the same quarter last year

- Free Cash Flow Margin: 7.8%, up from 5.8% in the same quarter last year

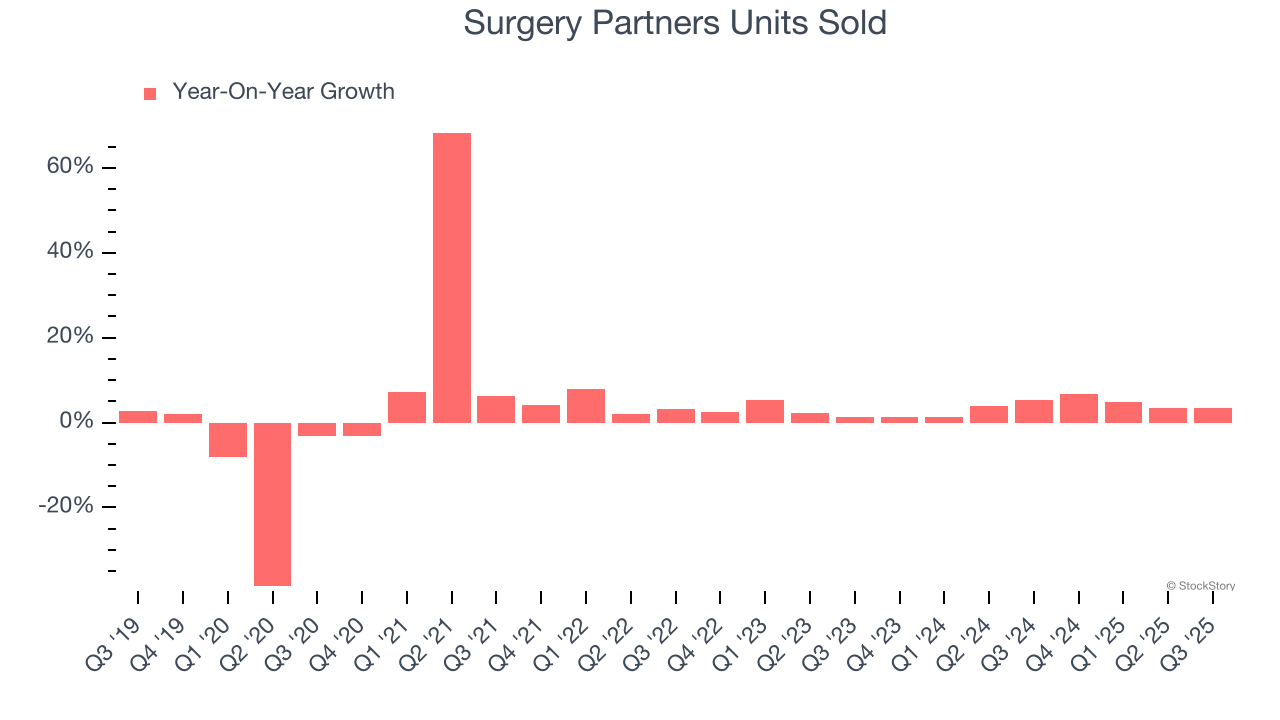

- Sales Volumes rose 3.4% year on year (5.4% in the same quarter last year)

- Market Capitalization: $2.74 billion

Company Overview

With more than 180 locations across 33 states serving as alternatives to traditional hospital settings, Surgery Partners (NASDAQ:SGRY) operates a national network of outpatient surgical facilities including ambulatory surgery centers and short-stay surgical hospitals.

Revenue Growth

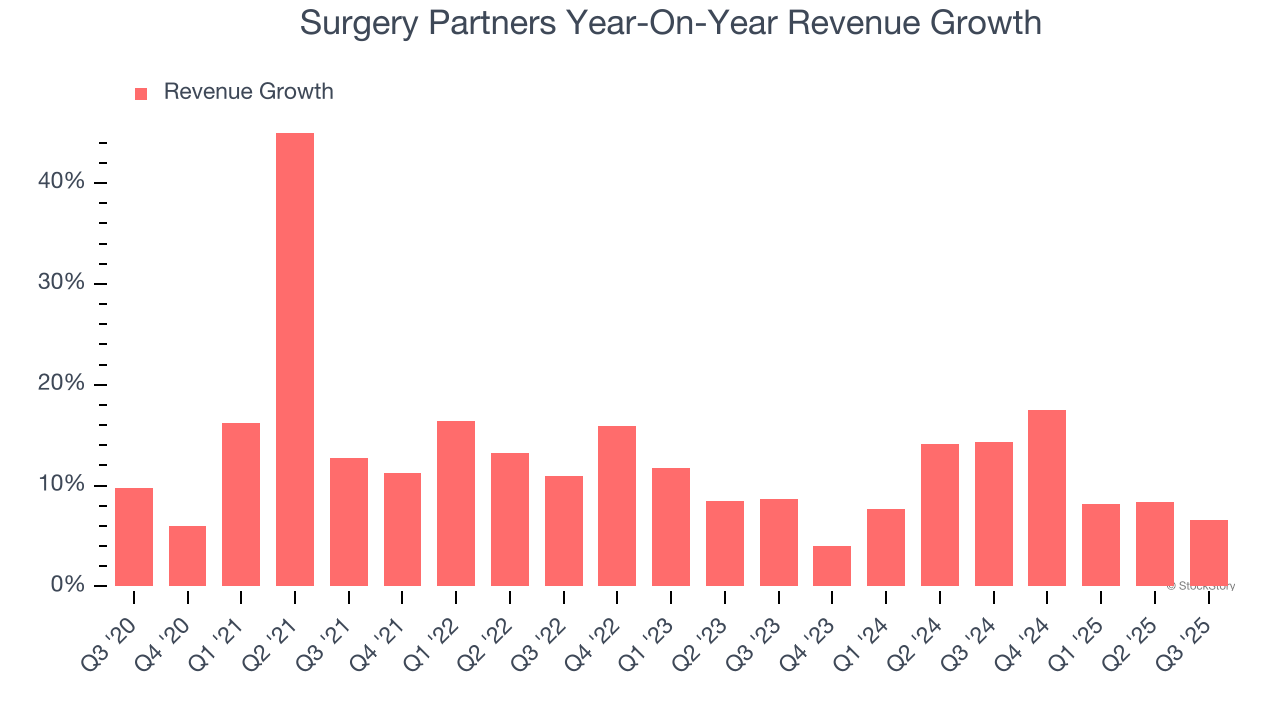

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Surgery Partners’s 12.4% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Surgery Partners’s annualized revenue growth of 10% over the last two years is below its five-year trend, but we still think the results were respectable.

Surgery Partners also reports its number of units sold. Over the last two years, Surgery Partners’s units sold averaged 3.8% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Surgery Partners grew its revenue by 6.6% year on year, and its $821.5 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.6% over the next 12 months, similar to its two-year rate. This projection is noteworthy and implies the market sees success for its products and services.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Surgery Partners’s operating margin has been trending up over the last 12 months and averaged 12.5% over the last five years. Its profitability was higher than the broader healthcare sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, Surgery Partners’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Surgery Partners generated an operating margin profit margin of 12.9%, up 5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Surgery Partners’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Surgery Partners reported adjusted EPS of $0.13, down from $0.19 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Surgery Partners’s full-year EPS of $0.78 to grow 28.6%.

Key Takeaways from Surgery Partners’s Q3 Results

We were impressed by how significantly Surgery Partners blew past analysts’ sales volume expectations this quarter. On the other hand, its EPS missed. Looking ahead, its full-year revenue and full-year EBITDA guidance both fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 13.5% to $18.61 immediately after reporting.

Surgery Partners didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.