Over the past six months, FirstSun Capital Bancorp’s shares (currently trading at $32.70) have posted a disappointing 11.3% loss, well below the S&P 500’s 15.3% gain. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy FirstSun Capital Bancorp, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Is FirstSun Capital Bancorp Not Exciting?

Even with the cheaper entry price, we're cautious about FirstSun Capital Bancorp. Here are three reasons we avoid FSUN and a stock we'd rather own.

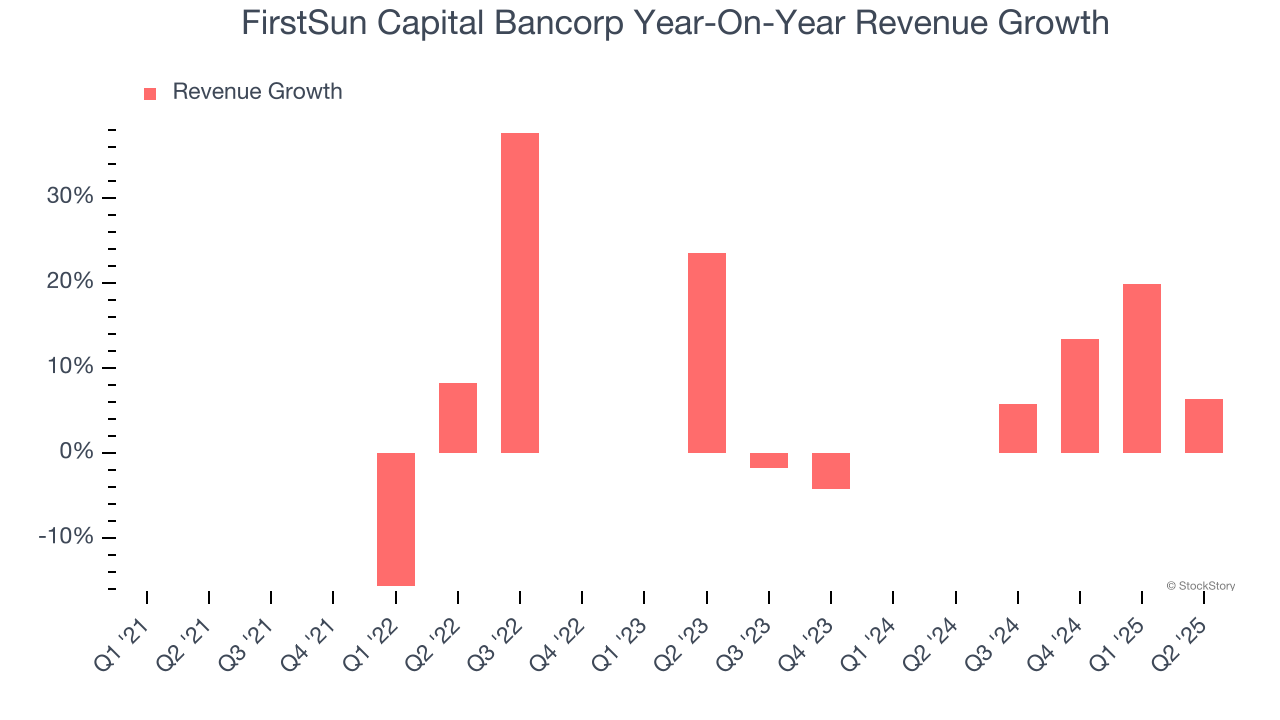

1. Lackluster Revenue Growth

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. FirstSun Capital Bancorp’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 2.9% over the last two years was well below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

2. Net Interest Margin Dropping

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, FirstSun Capital Bancorp’s net interest margin averaged 4.2%. However, its margin contracted by 22.3 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean FirstSun Capital Bancorp either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

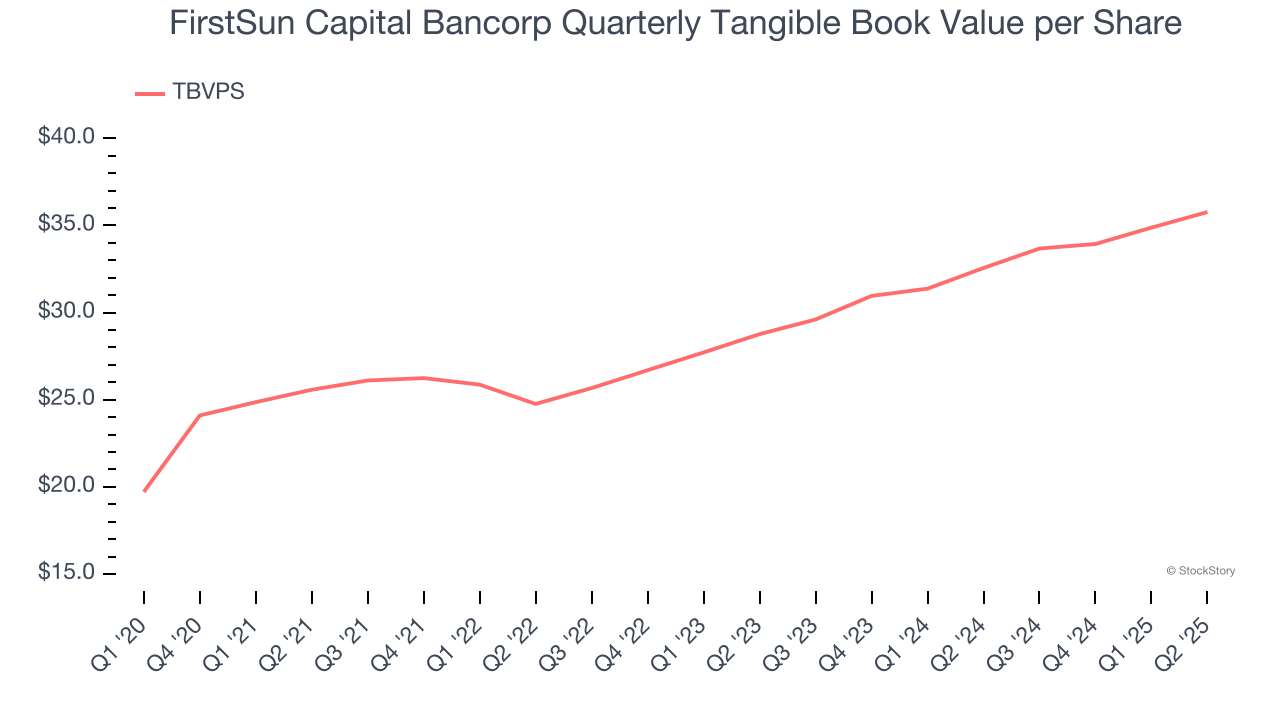

3. TBVPS Projections Show Stormy Skies Ahead

Tangible book value per share (TBVPS) growth comes from a bank’s ability to profitably lend while maintaining prudent risk management and efficient operations.

Over the next 12 months, Consensus estimates call for FirstSun Capital Bancorp’s TBVPS to shrink by 2.9% to $34.73, a sour projection.

Final Judgment

FirstSun Capital Bancorp isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 0.8× forward P/B (or $32.70 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now. We’d recommend looking at our favorite semiconductor picks and shovels play.

High-Quality Stocks for All Market Conditions

Fresh US-China trade tensions just tanked stocks—but strong bank earnings are fueling a sharp rebound. Don’t miss the bounce.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.